Market Update | First Quarter 2025

April 22, 2025

Key Highlights to Keep You Informed

U.S. equity markets peaked mid-February with the S&P 500 hitting a record 6,144.

Market volatility rose after 25% tariffs on Canadian and Mexican imports were announced on February 1ˢᵗ but quickly paused for 30 days. Meanwhile, 10% tariffs on Chinese imports took effect February 4ᵗʰ. After the February 18ᵗʰ market peak, officials signaled tariffs could rise to 25% on cars, semiconductors, and pharmaceuticals.

Markets remained volatile through the quarter amid tariff uncertainty, falling consumer confidence, and weak economic data ahead of the April 2ⁿᵈ “Liberation Day” trade announcement.

The selloff deepened in early April as a 10% universal import tariff and higher rates on targeted countries raised fears of retaliation and slower economic growth.

Despite some economic strength, consumer, and business confidence declined throughout the quarter.

Consumer confidence fell monthly, hitting 92.9, the lowest level since January 2021. The Expectations Index dropped to a 12-year low of 65.2, signaling recession fears driven by tariffs, inflation, and labor concerns. The NFIB small business optimism index also declined, ending the quarter at 97.4, below its 50-year average. Small business owners cited inflation and labor market challenges, not tariffs, as primary concerns.

The Atlanta Fed’s GDPNow tracker, which provides real-time GDP estimates, now projects a 2.4% contraction for Q1, down sharply from 2.4% growth in Q4 2024 and the first decline since 2022.

While the official estimate is still a month away and GDPNow tends to underestimate growth, it signals a clear slowdown. In contrast, the St. Louis Fed’s Nowcast still expects 2.01% growth, though GDPNow is typically more accurate late in the quarter.

Inflation data showed signs of easing throughout the quarter.

CPI rose 0.5% in January, pushing the annual rate to 3.0%, but February and March came in below expectations, bringing it down to 2.4%. The Fed’s preferred gauge, the PCE Price Index, also declined, holding at 2.5% through February. While this would typically support rate cuts, the Fed is likely to wait for more data and assess the impact of new tariffs.

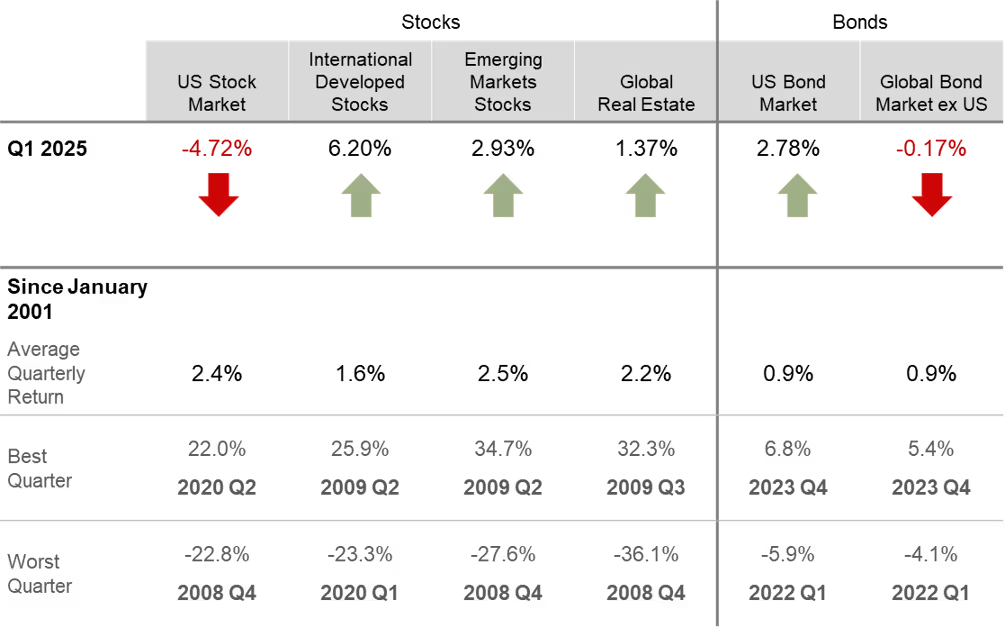

Quarterly Market Summary

Returns (USD), as of March 31, 2025

Past performance is not a guarantee of future results. Indices are not available for direct investment. Index performance does not reflect the expenses associated with the management of an actual portfolio. Market segment (index representation) as follows: US Stock Market (Russell 3000 Index), International Developed Stocks (MSCI World ex USA Index [net dividends]), Emerging Markets (MSCI Emerging Markets Index [net dividends]), Global Real Estate (S&P Global REIT Index [net dividends]), US Bond Market (Bloomberg US Aggregate Bond Index), and Global BondMarket ex US (Bloomberg Global Aggregate ex-USD Bond Index [hedged to USD]). S&P data © 2025 S&P Dow Jones Indices LLC, a division of S&P Global. All rights reserved. Frank Russell Company is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. MSCI data © MSCI 2025, all rights reserved. Bloomberg data provided by Bloomberg.

Notable Events in Q1

January

Chinese Artificial Intelligence (AI) company DeepSeek announced major breakthroughs, unveiling a model that rivaled U.S. counterparts at lower cost and resource use. This triggered a tech selloff, including a $600 billion drop in Nvidia’s valuation in one day. The “Magnificent 7” stocks have declined since, with losses accelerating on tariff news. Economic data showed signs of weakening as job growth, consumer spending, leading economic indicators, and service sector activity all posted weaker than expected readings. Inflation also ticked back up to 3.0%, breaking its downward trend. On a positive note, Israel and Hamas reached a ceasefire, including a hostage and prisoner exchange.

February

Early February saw a flurry of political activity as Tulsi Gabbard was confirmed as Director of National Intelligence, Robert F. Kennedy Jr. was confirmed as Health and Human Services Secretary, and Kash Patel was narrowly confirmed as the FBI Director. The month ended with a flare-up as well when a meeting between U.S. President Donald Trump and Ukrainian President Volodymyr Zelensky at the White House ended after a public argument.

March

In March, the U.S. imposed major tariffs, 25% on imports from Mexico and Canada (with Canadian energy products at 10%) and raised tariffs on Chinese goods from 10% to 20%. Though some tariffs were delayed, others remained, dispelling hopes they were only negotiation tactics. Aimed at curbing illegal immigration and drug trafficking, the move triggered retaliatory actions and heightened global trade tensions. Markets reacted with sharp volatility amid fears of inflation and a slowdown. Many companies lowered earnings forecasts due to weaker consumer spending and investment. After a brief recovery, markets fell again following a March 26th announcement of a 25% tariff on imported cars, pushing the S&P 500 to a six-month low and ending the quarter near year-to-date lows.

Economic Indicators

Economic data in the first quarter showed a somewhat conflicting story. From a feelings-based perspective, survey responses were negative. Consumer Confidencei and Consumer Sentimentii surveys both indicated that many are expecting a recession and foresee both higher inflation and unemployment this year. Despite the negative outlook, many felt OK about their present situation. The negative sentiment was primarily driven by tariff uncertainty and potential inflationary effects. Weakness was clearly felt in manufacturing reportsii, as they show a sector in or near contraction. Despite the gloomy mood, the employment market remains resilient—stronger than expected and able to keep many employediV. The service sector continues to expand, though there were signs of upward pricing pressuresv. Overall, the economy has been resilient and on better footing than soft data points indicated.

Much of the risk to the outlook is contingent upon the result of tariffs. As we have seen in the early stages of the second quarter, the tariffs announced were different than what anyone anticipated. Historically, tariffs have been an economic drag and have the potential to increase inflation. Looking ahead, there is still much uncertainty, as the health of the economy will likely depend on how long and to what extent tariffs persist. The Federal Reserve remains in a tough spot, as they are being pressured to cut interest rates, but they know there is a risk of higher inflation. In the short term, economic strength will depend on how consumers can navigate this environment. In the long term, we believe we will weather these events but will need to stay disciplined in the face of inevitable volatility.

i 2025 U.S. Economic Events&Analysis – Consumer Confidence, Econoday, 3/25/2025

ii 2025 U.S. Economic Events&Analysis – Consumer Sentiment, Econoday, 4/10/2025

iii2025 U.S. Economic Events&Analysis – PMI Manufacturing Final, Econoday, 4/1/2025

2025 U.S. Economic Events&Analysis – ISM Manufacturing Index, Econoday, 4/1/2025

iV2025 U.S. Economic Events&Analysis – Employment Situation, Econoday, 4/4/2025

v 2025 U.S. Economic Events&Analysis – PMI Composite Final, Econoday, 4/3/2025

2025 U.S. Economic Events&Analysis – ISM Services Index, Econoday, 4/3/2025

Market Impact on Major Asset Classes

Impact on Equities

In a reversal of a strong 2024, U.S. stocks measured by the S&P 500 fell 4.3% in the first quarter as uncertainty around tariffs and government policies weighed on sentiment. Absent the tariff threat, a pullback would not have been surprising given stocks have become more expensive, and the last 2 years have seen strong returns.

During the pullback, defensive stocks held up better as it was the relatively expensive and tech-heavy Nasdaq 100 that led the market lower with an 8.1% decline. Small cap stocks were down 9.5% as well.

Outside of the U.S., lower starting valuations, government stimulus, and dollar weakness led to market-leading returns. Developed international markets, measured by MSCI EAFE, were up 7%, with Europe up a particularly strong 10.6%. Fiscal spending in Europe was boosted by increased defense spending, given doubts about the U.S.’s willingness to intervene and protect others from foreign aggression.

The MSCI Japan return was flat, but the Japanese economy continues to improve, and the labor market is the strongest it has been since the 1990s. Tariffs are a risk to growth, but they do not export as much to the U.S. as many believe.

MSCI Emerging Markets also provided a decent 3% return. China led the broad index higher with a 15.1% return, as wage increases for government workers, as well as increased support for real estate and the banking system, helped the economy. Compared to inflationary risks in the U.S., deflation is the risk in China.

Looking ahead, there is clearly heightened uncertainty in the markets and expectations of heightened volatility. While we have gathered more information on the tariff stance, next steps are unpredictable, given the tariffs have seen several pauses and room for negotiation. In addition, there remains uncertainty around potential deregulation and tax cuts.

Given the backdrop, we continue to believe that diversification and balance will benefit investors, as the more expensive areas of the market have been prone to pullbacks when the economy falters. In fact, diversified portfolios have held up better in the first quarter compared to overall U.S. stock indexes that have grabbed headlines.

Moving forward, our team is taking a disciplined approach and seeking to avoid uncompensated risks in the market. Most importantly, it will be important to avoid emotional reactions and stick to a well-thought-out plan that was formulated with the thought in mind that disruptive periods like the current one will happen.

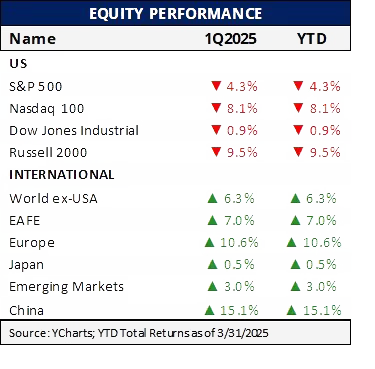

Major World Equity Market Performance for Q1 2025

Impact on Fixed Income

In the first quarter of 2025, the Bloomberg Barclays U.S. Aggregate Bond Index, a proxy for the U.S. bond market, managed a modest positive return. This performance was primarily driven by favorable inflation data and growing concerns about economic growth, which collectively enhanced the appeal of bonds. Notably, longer-duration bonds outperformed their shorter-duration counterparts, as investors sought higher long-term yields amid prevailing policy uncertainties.

Within the corporate bond sector, investment-grade bonds (characterized by higher quality but offering lower yields) surpassed the performance of their high-yield, lower-quality counterparts during the same period. This trend reflected investor apprehension regarding future economic growth in the context of ongoing policy uncertainties. Nevertheless, both investment-grade and high-yield corporate bonds concluded the quarter with modest gains, indicating a continued sense of economic optimism among bond investors.

Ongoing high levels of municipal bond issuance, combined with uncertainty surrounding the tax-exempt status of these bonds¹ (a very low probability outcome, in our view), put downward pressure on their prices. However, this also enhanced their relative attractiveness (higher yields), creating a more appealing opportunity for investors, especially those in high tax brackets with cash on the sidelines.

Overall, bond market volatility remained elevated during the quarter (particularly in March), as reflected by the Intercontinental Exchange (ICE) Bank of America Merrill Lynch Option Volatility Estimate (MOVE) Index. This was due to a combination of factors, including the uncertainty and variability associated with economic data (trending weaker) and global trade policies (tariffs). However, it’s important to remember that in the short term, bond returns can fluctuate with interest rates and credit spreads, but over time, they generally align with the yield at purchase.

Despite recent rate declines, current yields remain attractive by historical standards. Higher starting yields benefit investors in both rising and falling rate environments: boosting returns if prices rise and helping offset losses if rates increase.

Source:

¹ Government Finance Officers Association. (2025, January). Protecting bonds to build infrastructure and create jobs.

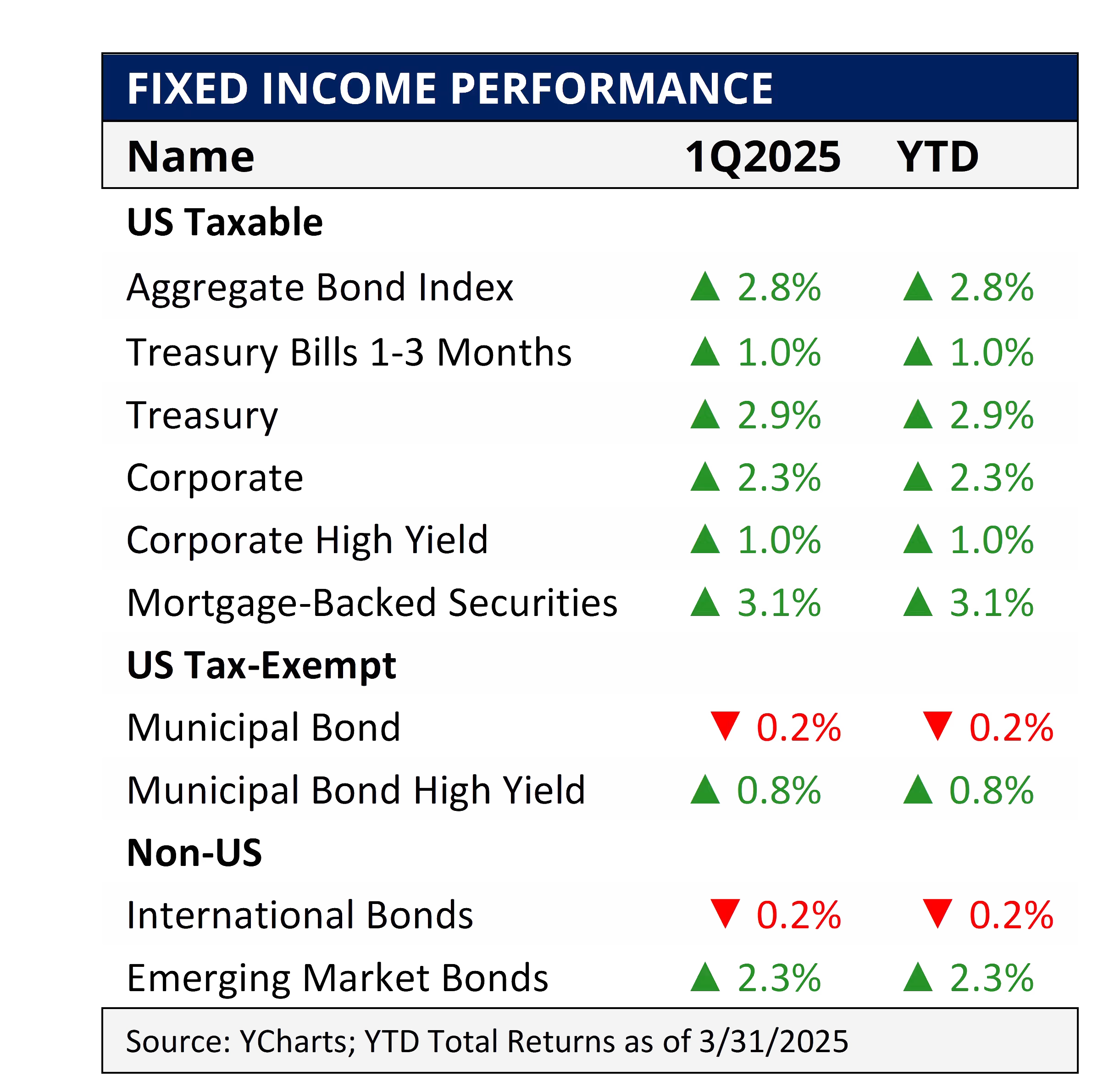

Major Fixed Income Index Returns for Q1 2025

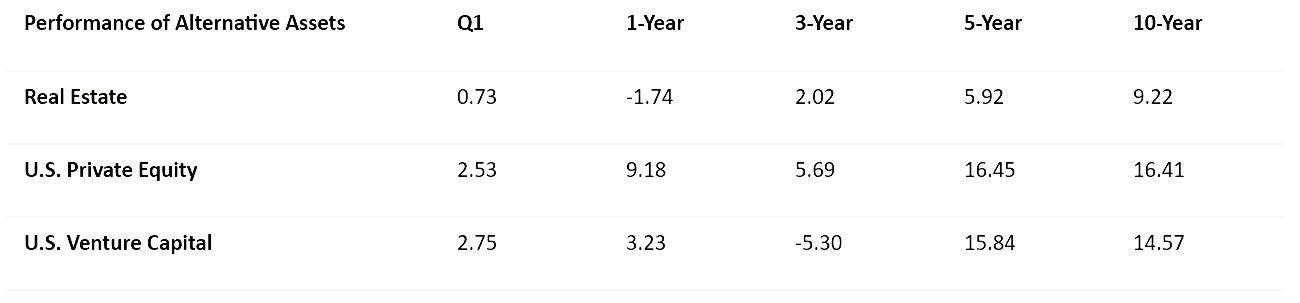

Impact on Alternatives

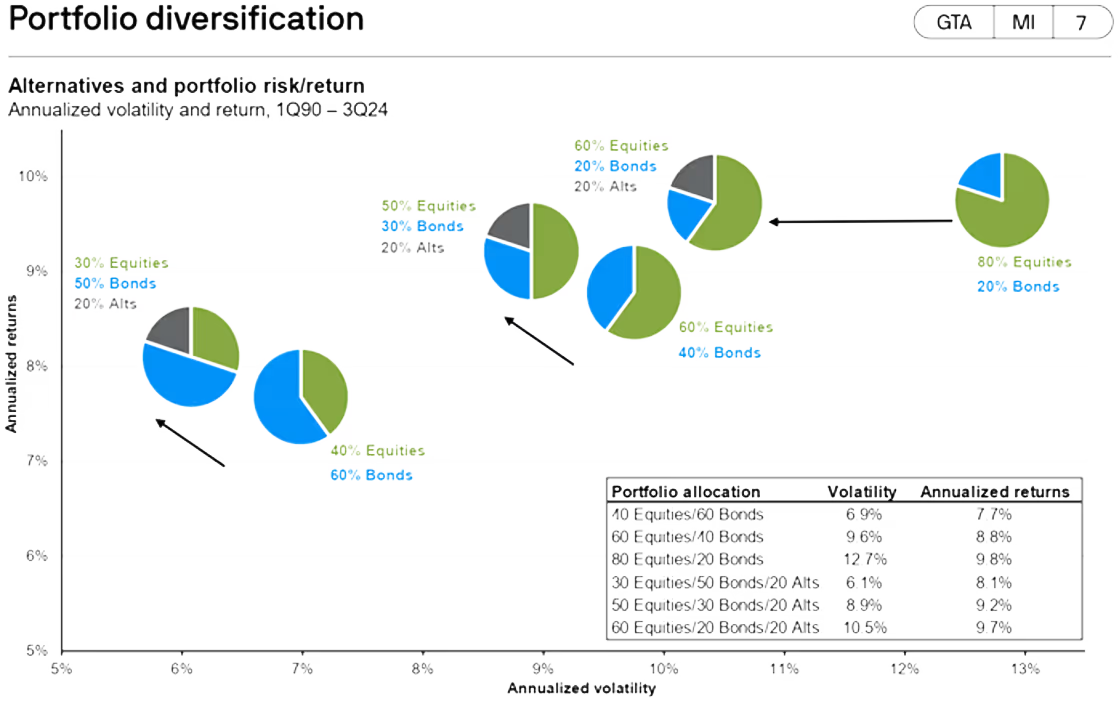

Increased volatility and lofty valuations highlight the need for diversification outside of traditional public markets. Adding a balance of alternative investments, including private equity, credit, and real assets, can help achieve this goal. Over the long term, through diverse market conditions, an allocation to alternatives has demonstrated the ability to reduce risk and increase return over traditional stock and bond portfolios.

Alternative investments can be grouped into return enhancers, such as private equity and private credit, which have demonstrated returns above public markets. The other benefit is increased diversification from real assets, such as real estate, infrastructure, and farmland, that have low correlations to public markets and can help during inflationary environments. Although an allocation to alternative investments can provide clear benefits, they also come with less liquidity than public market investments, creating a new set of risks.

Your TMG Wealth Advisor can help determine if alternatives are a fit and recommend an appropriate allocation and balance of funds to align with your individual risk tolerance.

Source: Bloomberg, Burgiss, HFRI, NCREIF, Standard & Poor’s, FactSet, J.P. Morgan Asset Management.

Performance of Alternative Assets

Alternative Investments carry a higher degree of risk related to illiquidity, valuation, and lack of a public market where they can be bought and sold. Investing in alternative investments carries the risk of loss to some or all of your principal investment.Alternative investments that fall under Rule 506 Regulation D of the Investment Company Act of 1940 (“the Act”) are considered unregistered funds, and therefore, are not regulated in the same way as a registered fund under the Act.Depending on the type of investment, a prospective investor must prequalify as an Accredited Investor or Qualified Purchaser under Rule 506, or as a Qualified Client defined under Rule 205-3 of the Investment Advisers Act of 1940, before investing.Please carefully review the investment’s Private Placement Memorandum (PPM) and/or other Offering Documents and Disclosures before investing in an alternative investment.

Looking Ahead

Volatility is and will likely remain at elevated levels as new economic policies are outlined, interest rate decisions are communicated by the Fed, and markets watch economic data releases over the coming months. The rebound in stocks on April 9th highlights the importance of remaining disciplined and avoiding emotional decision-making. The best days in markets are usually in close proximity to the worst days in markets. The 9.5% increase in the S&P 500 on April 9ᵗʰ was the third largest gain since the index became widely recognized. The two bigger gains were grouped around the global financial crisis in 2008, and unofficial records show larger gains around the period of the stock market crash in 1929 and the Great Depression.

While the future of economic policy and market conditions remains uncertain, and each market downturn may seem unique or unprecedented, history demonstrates that evidence-based investing and a disciplined strategy consistently outperform reactive trading. Although markets have reacted negatively to tariff discussions, we remain optimistic about fiscal stimulus through government spending and tax cuts, which are generally favorable for equities. Global diversification has proven beneficial this year, as international markets have outperformed domestic markets, and the U.S. dollar has weakened against other major currencies.

In the current market, value stocks have outperformed growth stocks, and incorporating alternative investments can further enhance diversification and optimize the risk-return balance. Regular portfolio rebalancing helps manage risk and keeps your strategy aligned with your objectives. By working together to reassess your strategy, we can position you for long-term success, helping you navigate any market environment with confidence and resilience.

Need more help?

Contact The Mather Group, your advisor, health insurance professional, or your state’s health insurance assistance program (SHIP) for additional information. SHIP is a national program that offers one-on-one Medicare counseling and assistance to individuals and their families.

Key Highlights to Keep You Informed

U.S. equity markets peaked mid-February with the S&P 500 hitting a record 6,144.

Market volatility rose after 25% tariffs on Canadian and Mexican imports were announced on February 1ˢᵗ but quickly paused for 30 days. Meanwhile, 10% tariffs on Chinese imports took effect February 4ᵗʰ. After the February 18ᵗʰ market peak, officials signaled tariffs could rise to 25% on cars, semiconductors, and pharmaceuticals.

Markets remained volatile through the quarter amid tariff uncertainty, falling consumer confidence, and weak economic data ahead of the April 2ⁿᵈ “Liberation Day” trade announcement.

The selloff deepened in early April as a 10% universal import tariff and higher rates on targeted countries raised fears of retaliation and slower economic growth.

Despite some economic strength, consumer, and business confidence declined throughout the quarter.

Consumer confidence fell monthly, hitting 92.9, the lowest level since January 2021. The Expectations Index dropped to a 12-year low of 65.2, signaling recession fears driven by tariffs, inflation, and labor concerns. The NFIB small business optimism index also declined, ending the quarter at 97.4, below its 50-year average. Small business owners cited inflation and labor market challenges, not tariffs, as primary concerns.

The Atlanta Fed’s GDPNow tracker, which provides real-time GDP estimates, now projects a 2.4% contraction for Q1, down sharply from 2.4% growth in Q4 2024 and the first decline since 2022.

While the official estimate is still a month away and GDPNow tends to underestimate growth, it signals a clear slowdown. In contrast, the St. Louis Fed’s Nowcast still expects 2.01% growth, though GDPNow is typically more accurate late in the quarter.

Inflation data showed signs of easing throughout the quarter.

CPI rose 0.5% in January, pushing the annual rate to 3.0%, but February and March came in below expectations, bringing it down to 2.4%. The Fed’s preferred gauge, the PCE Price Index, also declined, holding at 2.5% through February. While this would typically support rate cuts, the Fed is likely to wait for more data and assess the impact of new tariffs.

Quarterly Market Summary

Returns (USD), as of March 31, 2025

Past performance is not a guarantee of future results. Indices are not available for direct investment. Index performance does not reflect the expenses associated with the management of an actual portfolio. Market segment (index representation) as follows: US Stock Market (Russell 3000 Index), International Developed Stocks (MSCI World ex USA Index [net dividends]), Emerging Markets (MSCI Emerging Markets Index [net dividends]), Global Real Estate (S&P Global REIT Index [net dividends]), US Bond Market (Bloomberg US Aggregate Bond Index), and Global BondMarket ex US (Bloomberg Global Aggregate ex-USD Bond Index [hedged to USD]). S&P data © 2025 S&P Dow Jones Indices LLC, a division of S&P Global. All rights reserved. Frank Russell Company is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. MSCI data © MSCI 2025, all rights reserved. Bloomberg data provided by Bloomberg.

Notable Events in Q1

January

Chinese Artificial Intelligence (AI) company DeepSeek announced major breakthroughs, unveiling a model that rivaled U.S. counterparts at lower cost and resource use. This triggered a tech selloff, including a $600 billion drop in Nvidia’s valuation in one day. The “Magnificent 7” stocks have declined since, with losses accelerating on tariff news. Economic data showed signs of weakening as job growth, consumer spending, leading economic indicators, and service sector activity all posted weaker than expected readings. Inflation also ticked back up to 3.0%, breaking its downward trend. On a positive note, Israel and Hamas reached a ceasefire, including a hostage and prisoner exchange.

February

Early February saw a flurry of political activity as Tulsi Gabbard was confirmed as Director of National Intelligence, Robert F. Kennedy Jr. was confirmed as Health and Human Services Secretary, and Kash Patel was narrowly confirmed as the FBI Director. The month ended with a flare-up as well when a meeting between U.S. President Donald Trump and Ukrainian President Volodymyr Zelensky at the White House ended after a public argument.

March

In March, the U.S. imposed major tariffs, 25% on imports from Mexico and Canada (with Canadian energy products at 10%) and raised tariffs on Chinese goods from 10% to 20%. Though some tariffs were delayed, others remained, dispelling hopes they were only negotiation tactics. Aimed at curbing illegal immigration and drug trafficking, the move triggered retaliatory actions and heightened global trade tensions. Markets reacted with sharp volatility amid fears of inflation and a slowdown. Many companies lowered earnings forecasts due to weaker consumer spending and investment. After a brief recovery, markets fell again following a March 26th announcement of a 25% tariff on imported cars, pushing the S&P 500 to a six-month low and ending the quarter near year-to-date lows.

Economic Indicators

Economic data in the first quarter showed a somewhat conflicting story. From a feelings-based perspective, survey responses were negative. Consumer Confidencei and Consumer Sentimentii surveys both indicated that many are expecting a recession and foresee both higher inflation and unemployment this year. Despite the negative outlook, many felt OK about their present situation. The negative sentiment was primarily driven by tariff uncertainty and potential inflationary effects. Weakness was clearly felt in manufacturing reportsii, as they show a sector in or near contraction. Despite the gloomy mood, the employment market remains resilient—stronger than expected and able to keep many employediV. The service sector continues to expand, though there were signs of upward pricing pressuresv. Overall, the economy has been resilient and on better footing than soft data points indicated.

Much of the risk to the outlook is contingent upon the result of tariffs. As we have seen in the early stages of the second quarter, the tariffs announced were different than what anyone anticipated. Historically, tariffs have been an economic drag and have the potential to increase inflation. Looking ahead, there is still much uncertainty, as the health of the economy will likely depend on how long and to what extent tariffs persist. The Federal Reserve remains in a tough spot, as they are being pressured to cut interest rates, but they know there is a risk of higher inflation. In the short term, economic strength will depend on how consumers can navigate this environment. In the long term, we believe we will weather these events but will need to stay disciplined in the face of inevitable volatility.

i 2025 U.S. Economic Events&Analysis – Consumer Confidence, Econoday, 3/25/2025

ii 2025 U.S. Economic Events&Analysis – Consumer Sentiment, Econoday, 4/10/2025

iii2025 U.S. Economic Events&Analysis – PMI Manufacturing Final, Econoday, 4/1/2025

2025 U.S. Economic Events&Analysis – ISM Manufacturing Index, Econoday, 4/1/2025

iV2025 U.S. Economic Events&Analysis – Employment Situation, Econoday, 4/4/2025

v 2025 U.S. Economic Events&Analysis – PMI Composite Final, Econoday, 4/3/2025

2025 U.S. Economic Events&Analysis – ISM Services Index, Econoday, 4/3/2025

Market Impact on Major Asset Classes

Impact on Equities

In a reversal of a strong 2024, U.S. stocks measured by the S&P 500 fell 4.3% in the first quarter as uncertainty around tariffs and government policies weighed on sentiment. Absent the tariff threat, a pullback would not have been surprising given stocks have become more expensive, and the last 2 years have seen strong returns.

During the pullback, defensive stocks held up better as it was the relatively expensive and tech-heavy Nasdaq 100 that led the market lower with an 8.1% decline. Small cap stocks were down 9.5% as well.

Outside of the U.S., lower starting valuations, government stimulus, and dollar weakness led to market-leading returns. Developed international markets, measured by MSCI EAFE, were up 7%, with Europe up a particularly strong 10.6%. Fiscal spending in Europe was boosted by increased defense spending, given doubts about the U.S.’s willingness to intervene and protect others from foreign aggression.

The MSCI Japan return was flat, but the Japanese economy continues to improve, and the labor market is the strongest it has been since the 1990s. Tariffs are a risk to growth, but they do not export as much to the U.S. as many believe.

MSCI Emerging Markets also provided a decent 3% return. China led the broad index higher with a 15.1% return, as wage increases for government workers, as well as increased support for real estate and the banking system, helped the economy. Compared to inflationary risks in the U.S., deflation is the risk in China.

Looking ahead, there is clearly heightened uncertainty in the markets and expectations of heightened volatility. While we have gathered more information on the tariff stance, next steps are unpredictable, given the tariffs have seen several pauses and room for negotiation. In addition, there remains uncertainty around potential deregulation and tax cuts.

Given the backdrop, we continue to believe that diversification and balance will benefit investors, as the more expensive areas of the market have been prone to pullbacks when the economy falters. In fact, diversified portfolios have held up better in the first quarter compared to overall U.S. stock indexes that have grabbed headlines.

Moving forward, our team is taking a disciplined approach and seeking to avoid uncompensated risks in the market. Most importantly, it will be important to avoid emotional reactions and stick to a well-thought-out plan that was formulated with the thought in mind that disruptive periods like the current one will happen.

Major World Equity Market Performance for Q1 2025

Impact on Fixed Income

In the first quarter of 2025, the Bloomberg Barclays U.S. Aggregate Bond Index, a proxy for the U.S. bond market, managed a modest positive return. This performance was primarily driven by favorable inflation data and growing concerns about economic growth, which collectively enhanced the appeal of bonds. Notably, longer-duration bonds outperformed their shorter-duration counterparts, as investors sought higher long-term yields amid prevailing policy uncertainties.

Within the corporate bond sector, investment-grade bonds (characterized by higher quality but offering lower yields) surpassed the performance of their high-yield, lower-quality counterparts during the same period. This trend reflected investor apprehension regarding future economic growth in the context of ongoing policy uncertainties. Nevertheless, both investment-grade and high-yield corporate bonds concluded the quarter with modest gains, indicating a continued sense of economic optimism among bond investors.

Ongoing high levels of municipal bond issuance, combined with uncertainty surrounding the tax-exempt status of these bonds¹ (a very low probability outcome, in our view), put downward pressure on their prices. However, this also enhanced their relative attractiveness (higher yields), creating a more appealing opportunity for investors, especially those in high tax brackets with cash on the sidelines.

Overall, bond market volatility remained elevated during the quarter (particularly in March), as reflected by the Intercontinental Exchange (ICE) Bank of America Merrill Lynch Option Volatility Estimate (MOVE) Index. This was due to a combination of factors, including the uncertainty and variability associated with economic data (trending weaker) and global trade policies (tariffs). However, it’s important to remember that in the short term, bond returns can fluctuate with interest rates and credit spreads, but over time, they generally align with the yield at purchase.

Despite recent rate declines, current yields remain attractive by historical standards. Higher starting yields benefit investors in both rising and falling rate environments: boosting returns if prices rise and helping offset losses if rates increase.

Source:

¹ Government Finance Officers Association. (2025, January). Protecting bonds to build infrastructure and create jobs.

Major Fixed Income Index Returns for Q1 2025

Impact on Alternatives

Increased volatility and lofty valuations highlight the need for diversification outside of traditional public markets. Adding a balance of alternative investments, including private equity, credit, and real assets, can help achieve this goal. Over the long term, through diverse market conditions, an allocation to alternatives has demonstrated the ability to reduce risk and increase return over traditional stock and bond portfolios.

Alternative investments can be grouped into return enhancers, such as private equity and private credit, which have demonstrated returns above public markets. The other benefit is increased diversification from real assets, such as real estate, infrastructure, and farmland, that have low correlations to public markets and can help during inflationary environments. Although an allocation to alternative investments can provide clear benefits, they also come with less liquidity than public market investments, creating a new set of risks.

Your TMG Wealth Advisor can help determine if alternatives are a fit and recommend an appropriate allocation and balance of funds to align with your individual risk tolerance.

Source: Bloomberg, Burgiss, HFRI, NCREIF, Standard & Poor’s, FactSet, J.P. Morgan Asset Management.

Performance of Alternative Assets

Alternative Investments carry a higher degree of risk related to illiquidity, valuation, and lack of a public market where they can be bought and sold. Investing in alternative investments carries the risk of loss to some or all of your principal investment.Alternative investments that fall under Rule 506 Regulation D of the Investment Company Act of 1940 (“the Act”) are considered unregistered funds, and therefore, are not regulated in the same way as a registered fund under the Act.Depending on the type of investment, a prospective investor must prequalify as an Accredited Investor or Qualified Purchaser under Rule 506, or as a Qualified Client defined under Rule 205-3 of the Investment Advisers Act of 1940, before investing.Please carefully review the investment’s Private Placement Memorandum (PPM) and/or other Offering Documents and Disclosures before investing in an alternative investment.

Looking Ahead

Volatility is and will likely remain at elevated levels as new economic policies are outlined, interest rate decisions are communicated by the Fed, and markets watch economic data releases over the coming months. The rebound in stocks on April 9th highlights the importance of remaining disciplined and avoiding emotional decision-making. The best days in markets are usually in close proximity to the worst days in markets. The 9.5% increase in the S&P 500 on April 9ᵗʰ was the third largest gain since the index became widely recognized. The two bigger gains were grouped around the global financial crisis in 2008, and unofficial records show larger gains around the period of the stock market crash in 1929 and the Great Depression.

While the future of economic policy and market conditions remains uncertain, and each market downturn may seem unique or unprecedented, history demonstrates that evidence-based investing and a disciplined strategy consistently outperform reactive trading. Although markets have reacted negatively to tariff discussions, we remain optimistic about fiscal stimulus through government spending and tax cuts, which are generally favorable for equities. Global diversification has proven beneficial this year, as international markets have outperformed domestic markets, and the U.S. dollar has weakened against other major currencies.

In the current market, value stocks have outperformed growth stocks, and incorporating alternative investments can further enhance diversification and optimize the risk-return balance. Regular portfolio rebalancing helps manage risk and keeps your strategy aligned with your objectives. By working together to reassess your strategy, we can position you for long-term success, helping you navigate any market environment with confidence and resilience.

Need more help?

Contact The Mather Group, your advisor, health insurance professional, or your state’s health insurance assistance program (SHIP) for additional information. SHIP is a national program that offers one-on-one Medicare counseling and assistance to individuals and their families.

.avif)